11 / 12

11 / 12

Upcoming changes | 11

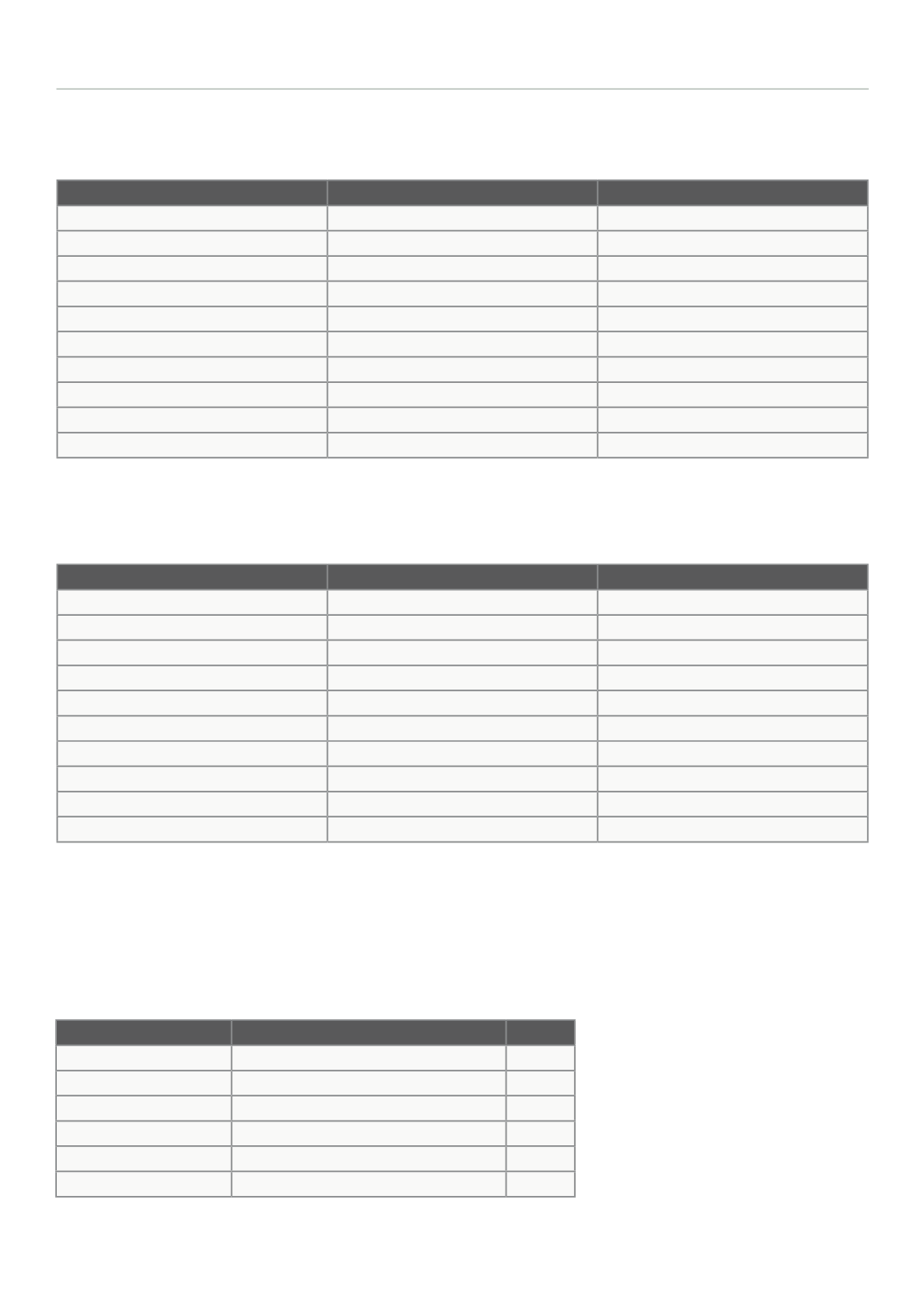

Band

Taxable income 2018/19

Rate*

Personal allowance** Up to £11,850

0%

Starter rate***

£11,851 to £13,850

19%

Basic rate

£13,851 to £24,000

20%

Intermediate rate***

£24,001 to £43,430

21%

Higher rate

£43,431 to £150,000

41%

Top rate

Above £150,000

46%

Table 3 - Scotland

Non-savings, non-dividend.

The personal allowance is reduced

by £1 for each £2 of income from

£100,000 to £123,700 (2017/18,

£123,000).

Indicates the two new bands being

introduced.

2018/19

2017/18

Starting rate* of 0% on savings up to

£5,000

£5,000

Basic rate band

£34,500

£33,500

Higher rate band

£34,501 - £150,000

£33,501 - £150,000

Additional rate band

Over £150,000

Over £150,000

Basic rate

20%

20%

Higher rate

40%

40%

Additional rate

45%

45%

Dividend ordinary rate

7.5%

7.5%

Dividend upper rate

32.5%

32.5%

Dividend additional rate

38.1%

38.1%

2018/19

2017/18

Personal allowance*

£11,850

£11,500

Personal savings allowance:

Basic rate taxpayer

£1,000

£1,000

Higher rate taxpayer

£500

£500

Dividend allowance

£2,000

£5,000

Marriage allowance**

£1,185

£1,150

Trading allowance***

£1,000

£1,000

Property allowance***

£1,000

£1,000

Rent a room allowance

£7,500

£7,500

Blind person’s allowance

£2,390

£2,320

Table 1 - Taxable income bands and tax rates

Table 2 - Allowances that reduce taxable income or are not taxable

* The starting rate does not apply if taxable non-saving income exceeds the starting rate limit.

The personal allowance is reduced by £1 for each £2 of income from £100,000 to £123,700 (2017/18, £123,000).

Any unused personal allowance maybe transferred to a spouse or civil partner who is not liable to higher or additional rate tax.

Note that landlords and traders with gross income from this source in excess of £1,000 can deduct the allowance

from their gross income as an alternative to claiming expenses.

*

**

***

*

**

***