Financial planning for businesses

Consider how likely you are to make

a sale based on:

•

your market share

•

resources (including staff)

•

prices

•

barriers to making sales

•

your products

•

marketing and advertising plans

•

legislation changes.

This information might be difficult to

predict for new businesses. However,

it gets easier over time as you can use

figures from previous months and years

to build a more accurate picture of how

much you expect to sell.

New businesses can compare start-up

costs against sales forecasts to get an

indication of the viability of their business

idea. If start-up costs outweigh expected

revenue, you will need to think of ways

to sell more, reduce costs or find a more

feasible business idea.

Expenditure forecast

The second part of the profit and loss

account is the expenditure forecast. This

provides the insight you must have in order

to establish how profitable you might be.

Best projected on a monthly basis, an

expenditure forecast includes:

•

expected sales

•

cost of sales

•

gross profit margin

•

expenditure – the overheads

•

projected net profit.

Compare expected figures with the

actual figures to see discrepancies

in your forecasts and where you can

make savings.

Limited companies have to supply HMRC

with a profit and loss statement as part of

their annual statutory accounts.

Cashflow forecasts

Every business, no matter how profitable,

needs to make sure there is enough

money coming in to pay the bills on

time. A cashflow forecast is a list of

business expenditure and income. It

lets you see easily when you will have a

shortfall or surplus of cash and allows

you to plan accordingly.

Cashflow forecasts can be complied

monthly or weekly depending on the

needs of the business. Things to take into

account may include:

An accurate cashflow forecast will

help you:

•

avoid running into financial problems

•

identify potential trouble spots

•

have a clear view of what lies ahead.

Good cashflow is not necessarily an

indication of healthy profits. A business

can be profitable but suffer from cashflow

problems at the same time, and vice versa.

A business with good cashflow will have

funds available to cover periods between

cash going out of and coming into the

business. A business might also consider

having cash reserves and access to

an overdraft in case of an unexpected

shortfall.

Maintaining a good cashflow is

particularly important in the early stages

of a business when your outgoings are

likely to exceed your incomings. You

will need to consider monthly, quarterly,

annual and one-off costs when working

out your cashflow.

Finance for

established

businesses

Businesses seek external funding for a

variety of reasons. If your business is

doing well, you might need to raise cash

to fund expansion. Or perhaps you might

need some additional funding to survive a

rough patch.

Either way, there’s no magic formula to

convince a bank to lend you money or an

investor to believe in you. However, there

are some practical ways you can enhance

your chances of securing business finance:

•

Business plans are not just for start-

ups. Keep your business plan up to

date to show investors that you know

what you are doing and have a plan

in place to realise your goals.

•

Keeping your paperwork in order

will make the process of applying for

funding much simpler and will give

potential lenders all the information

they need straightaway. Banks might

want to see historical data as well as

recent figures.

•

Use your profit and loss and cashflow

forecasts to your advantage. These

projections can demonstrate your

ability to pay back a loan.

•

Prepare periodic management

accounts in order to keep track of the

actual results compared to forecast.

Checklist: 6 point

business plan

1. Executive summary

An overview of the business

you want to start and run.

2. The business opportunity

What you plan to sell or offer and

who your customers will be.

3. Sales and marketing strategy

The need for your business and

how you plan to sell your product

or service.

4. The people involved

Your experience and the people

you want to work with.

5. Operations

Where the business will be based

and equipment you need.

6. Financial forecasts

How the business will work financially.

We can help

We can help you put together business

plans, applications for finance and

forecasts for all areas of your business

finances. Contact us today to talk about

your business.

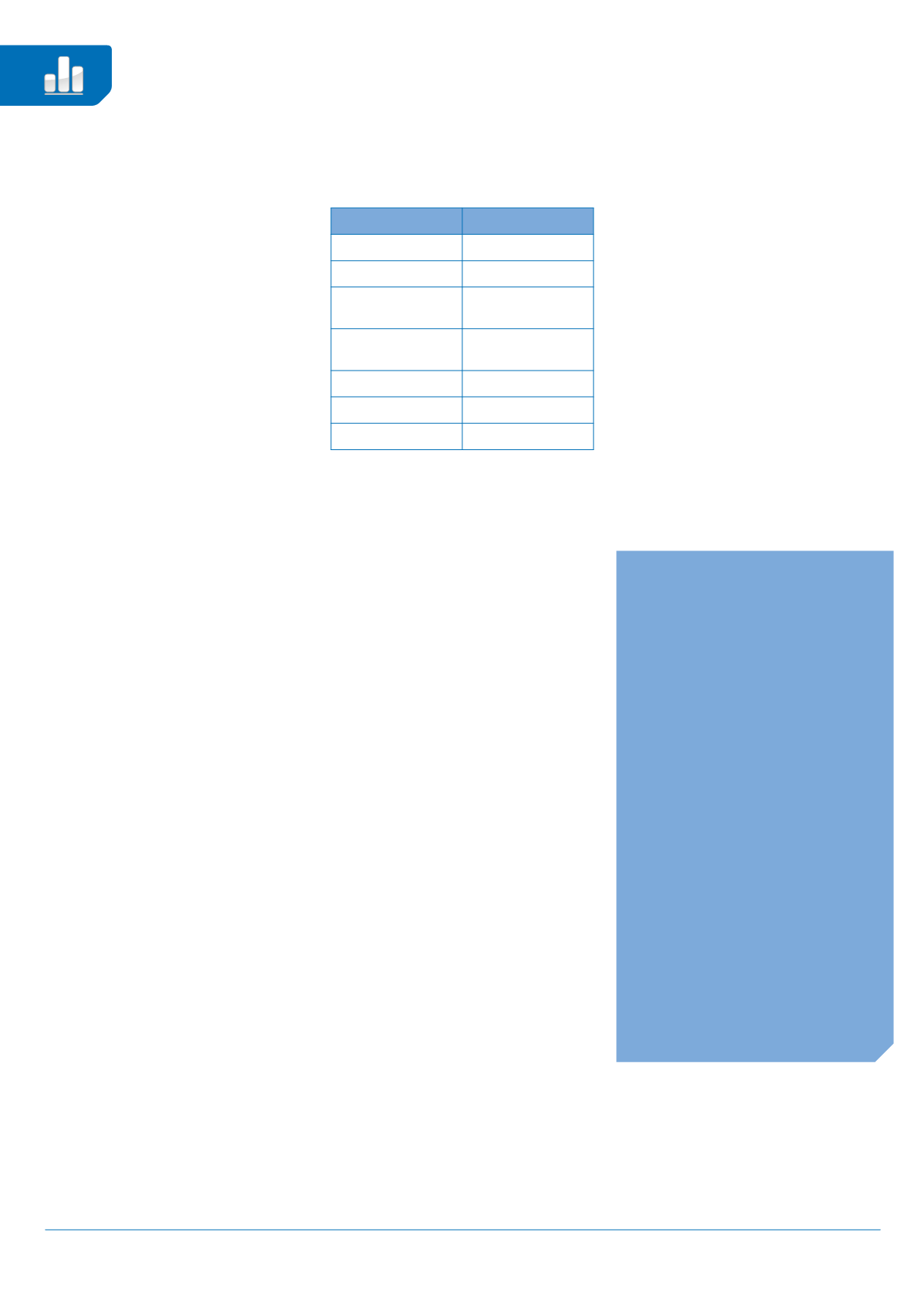

Expenditure

Income

Stock and materials

Sales

Equipment

Interest on savings

Wages, rent and

utilities

Bank loans

Running costs

Shareholder and/or

director investments

Loan repayments

Dividend payments

Tax on profits